Key Points:

- There were 7.4 million job openings nationwide in April, according to the Bureau of Labor Statistics, up from an upwardly revised 7.2 million in March and above consensus expectations.

- The national quits rate was largely steady at 2%

- The layoff rate in April was 1.1%, up very slightly from 1% in March.

April’s job openings data was surprisingly decent, defying expectations for more deterioration in the face of the whipsaw on-again/off-again tariff and trade developments that characterized much of the month. The data suggest that US employers maintained at least enough confidence to keep more jobs open in April than they had in March, whether through careful planning, strong and adaptable supply chains and/or a good amount of luck. But just because employers managed to skate through one month does not ensure they will be able to do so indefinitely, especially as uncertainty and volatility remain heightened. The market remains distressingly gridlocked, with limited hiring and low quits, and the market can’t keep steadily cooling off forever before it just turns cold.

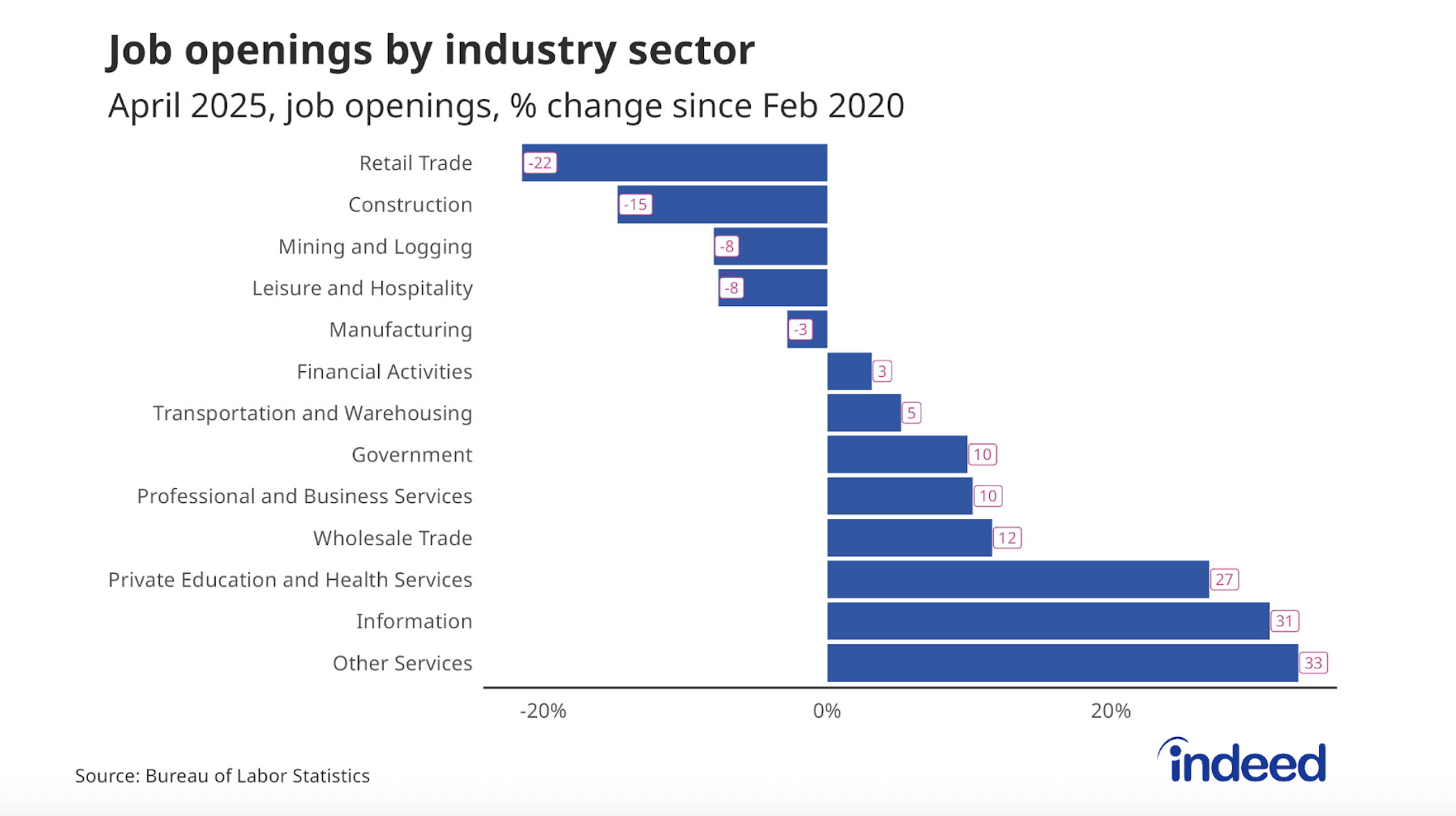

On a sector level, there’s more change under the surface than expected. Sectors that were darlings of the post pandemic recovery period, including retail trade, leisure and hospitality and manufacturing are now lagging behind. And sectors that have borne the brunt of the labor market slowdown of the past few years, including information and professional business services, have started picking up. An increase in business services roles – which typically require somewhat longer and more dedicated planning and commitment – could indicate businesses are more confident than expected. On the other hand, a pullback in sectors more reliant on discretionary spending, including retail and accommodation, could indicate an emerging caution on the part of consumers, which may be a signal for what’s to come.

Today’s data is likely to reinforce the Federal Reserve’s decision to keep key federal interest rates unchanged. The labor market remains in good-but-not-great shape, inflation continues to remain subdued and the economy so far has generally taken the heightened volatility and uncertainty of the past few months in stride. Whether that can continue is the most pressing question. Optimists can point to better-than-expected growth in job openings and limited layoffs as things worth feeling good about. Pessimists will focus on the ongoing difficulty of traditional business planning in the face of policy whiplash, and will have plenty of fuel to doubt how long current conditions can last. The backwards-looking nature of this data only contributes to the cloudy view ahead, and the May jobs report data coming later this month will hopefully provide a clearer picture of what has been and what’s to come.